Initially, the Fiscal Responsibility Act was enacted at the national level, in 2003 with the primary objectives being, to decrease Government's fiscal deficits and increase transparency in the functioning.

This act was then initiated by different State Governments and here we look at the Gujarat Fiscal Responsibility Act, passed in 2005.

The Fiscal Responsibility Act directs the State Government of Gujarat to reduce its fiscal deficits, conduct the fiscal operations with greater transparency and lay down Medium Term Fiscal Responsibility Statement and Fiscal Policy Strategy Statement annually.

To understand the term Fiscal Deficit, we must first understand what fiscal means and two general terms, expenditure and receipt.

Fiscal: This term signifies the relation to taxation or revenue.

Both these terms are used when the government puts forward the annual budget and they comprise two factors, capital and revenue.

Expenditure: This refers to the revenue and capital disbursements of different ministries and departments. It is the value spent by the government for public welfare in terms of capital and revenue.

Receipt: This is the method in which the government procures resources of revenue and capital.

Fiscal deficit:

It is the difference between the total expenditure and the total receipt of the Government. This means that the government is spending more on revenue and capital than is being generated.

This pushes the government into a deficit termed as 'fiscal deficit'.

The Fiscal Responsibility Act directs the State Government to present an annual Medium Term Fiscal Policy Statement and the Fiscal Policy Strategy Statement Along With the budget.

The purpose is to reduce the fiscal deficit and the revenue deficit of the State.

The Medium Term Fiscal Policy Statement:

The Medium Term Fiscal Policy Statement and the Fiscal Policy Strategy Statement provide the objectives and the strategies the State Government would bring forth, to fulfill these objectives. They also give a three years rolling target for managing the fiscal Liabilities.

The Medium Term Fiscal Policy Statement also includes the assessment of revenue deficit, that is, the difference between revenue receipt and revenue expenditure,

The capital acquired by the state which would be used for producing assets and,

The estimated yearly pension liabilities worked out on an actuarial basis (a method in which risks are calculated to predict future events and take preventive measures using probability and statistics), for the next ten years.

The Fiscal Policy Strategy Statement contains :

The policies of the State Government for the ensuing financial year in the matters of taxation, expenditure, borrowings, lending and investments,

how the government would set the price of goods and services and a description of the guarantees provided by the Government.

Along with these policies, the Fiscal Policy Strategy Statement should also outline the measures to be taken by the Government, its strategies, in order to Control fiscal deficits in the ensuing financial year.

The government should also explain the reason if there is any deviation in the strategies adopted from those laid out in the Strategy policy.

Comparison of the fiscal policies of the State with the Fiscal management principles and evaluation whether they align with the principles or not.

Evaluation of the performance in the previous year and the expected results in the current year.

Fiscal management principles-

Under the Fiscal Management Principles, the State Government. Is directed to,

(1) Take appropriate measures to reduce the revenue and fiscal deficits.

(2) Create a revenue surplus which then can be utilized for discharging liabilities of the State.

(3) Follow the following Fiscal management principles:

The government shall be:

Transparent in setting the fiscal policy objectives, in the implementation of public policy and in the publication of public accounts

There should be stability in the fiscal policy making process.

Public finances should be managed in a responsible manner.

Fair in its policy making, keeping in mind the implications on future generations.

The Fiscal Policy should be efficiently designed and managed to optimize the outputs.

Maintain the government debt at prudent levels and manage guarantees and liabilities of the Government prudently

Ensure integrity of the tax system and also start non tax revenue policies to promote cost recovery and equity.

Implement expenditure policies which promote economic growth, poverty reduction and welfare of the people.

Utilize public assets in the best manner

Minimize the financial risks associated with public sector undertaking to save finances and use them for providing public services.

Targets of the Fiscal Management Policy:

Reduce the revenue deficit to zero within a time period of three years commencing from 1st April, 2005 and ending on 31st March, 2008.

Reduce the fiscal deficit to not more than 3% of the Gross State Domestic Product within a period of four years

To limit the total public debt of the state government to 30% of the Gross State Domestic Product of the third year, within a span of 3 years.

To limit the outstanding guarantees to the level set by the Gujarat State Guarantees Act, 1963.

The act also mentions the level of revenue and fiscal deficits may exceed the set limit in case of any unforeseen conditions like natural calamities.

This is called the escape clause which provides a way for the government to protect itself from undeserved criticism in the scenario an extreme situation comes about.

Measures for transparency:

The State Government should also take measures to ensure Transparency in its functioning:

and formulation of the budget.

This being said, the government may reserve information which would adversely affect the interest of the state exchequer.

The government should also disclose the following points at the time of presentation of the budget:

Any significant changes in policies and practices which would affect the calculation of fiscal indicators.

The liabilities created as a result of guarantees, actual liabilities which Come from the borrowing of money by Public Sector Undertakings, Special purpose vehicles and other instruments where the liability of repayment is on the State government.

Revenue demands which were raised but not realized.

The estimated yearly pension liabilities, which are worked out on an actual basis, for the next ten years.

Measures to Enforce Compliance:

Under this section of the Act,

The budget presented and the policies announced at the time of the budget should be consistent with the objectives of the Medium Term Fiscal Policy Statement and the Fiscal Policy Strategy Statement and the Fiscal Management Targets.

Moreover, any triggers which can occur and the actions to be taken in case the triggers are activated should be mentioned in the budget.

The Finance Minister of the State would review the current trends in receipts and expenditure with respect to the budget and mention the remedial measures required to be taken to achieve the budget targets. The report of this review should be placed before the State Legislature during the session immediately following the end of the second quarter of the financial year.

The review report mentioned above should comprise:

any deviation or likely deviation in meeting the obligations cast on the State Government under this Act.

whether such deviation is substantial, and how much of the deviation can be attributed to general economic environment and to policy changes by the Government;

the remedial measures which the State Government proposes to take;

whenever there is a prospect of either shortfall in revenue or excess of expenditure over the budgetary provisions for a given year on account of any new policy decision of the State Government that affects either the Government or public sector undertakings, the Government, prior to taking such policy decisions, shall take measures to fully offset the fiscal impact for the current and future years by curtailing the sums authorized to be paid and applied from and out of the Consolidated Fund of the State under any Act to provide for the appropriations of such sums or by taking interim measures for revenue augmentation, or by taking up a combination of both:

Provided that nothing in this subsection shall apply to the expenditure charged on the Consolidated Fund of the State under clause (3) of article 202 of the Constitution of India.

In case the revenue deficit and fiscal deficit exceed on account of unforeseen demands on the finances of the Government, the Government shall identify the net fiscal cost of the calamity and such cost would provide ceiling for extent of non-compliance to the specified limits

Whenever, one or more supplementary estimates are presented in the State Legislature, the State Government shall also present an accompanying statement indicating the corresponding curtailment of expenditure and augmentation of revenue to fully offset the fiscal impact of the supplementary estimates in relation to the budget targets of the current year and the objectives of the Medium Term Fiscal Policy Statement, Fiscal Policy Strategy Statement and the Fiscal Management Targets for the future year.

Power to make Rules:

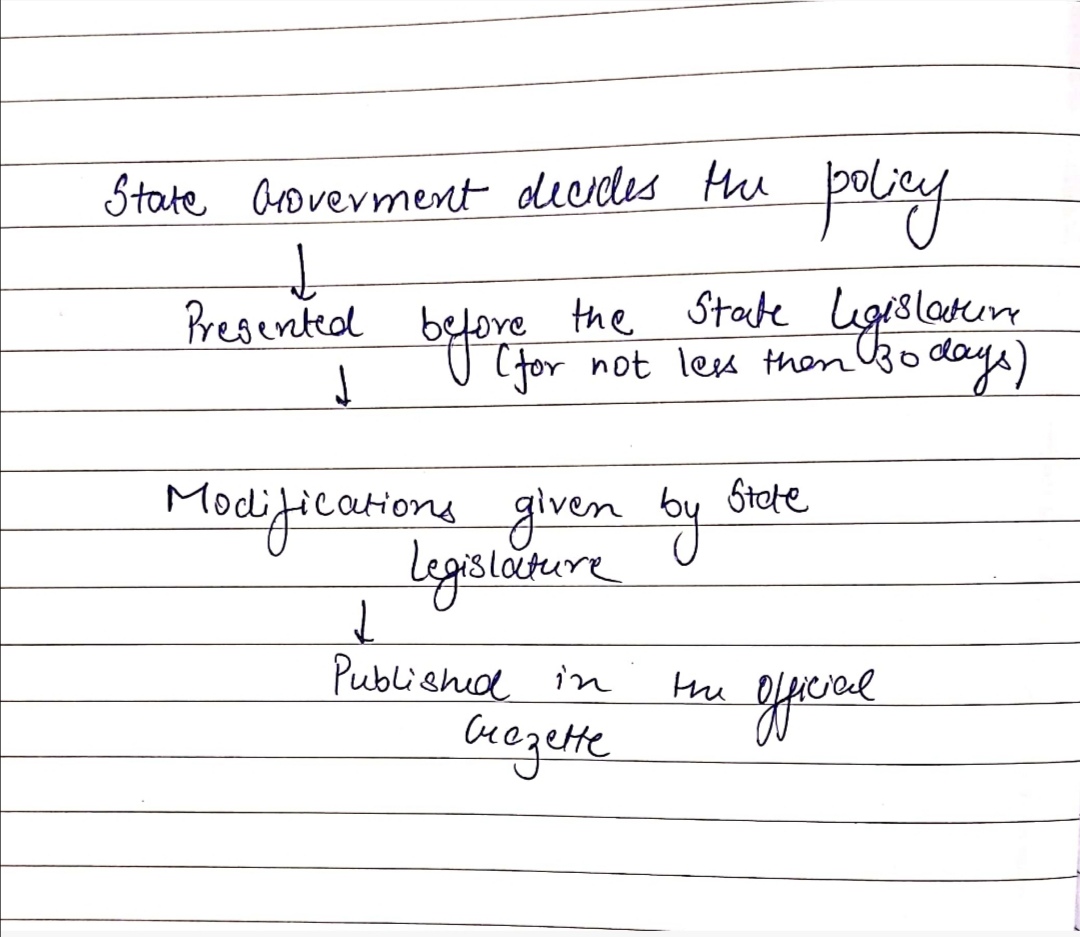

The State Government has the power to make Rules for carrying out the purposes of the Fiscal Responsibility Act, which it has to notify in the Official Gazette.

These rules may be regarding the following matters:

the measures of evaluation of Fiscal position of the State Government.

the form of Medium Term Fiscal Policy Statement and Fiscal Policy Strategic Statement

any other matter which is required to be, or may be prescribed.

All rules made under this section shall be laid for not less than thirty' days before the State Legislature as soon as may be after they are made, and shall be subject to rescission by the State Legislature or to such modifications

Any rescission or modification so made by the State Legislature shall be published in the Official Gazette and shall thereupon take effect.

Protection of Action Taken in Good Faith:

No suit, prosecution or other legal proceedings shall lie against the State Government or any officer of the Government for anything which is in good faith done or intended to be done under this Act or the rules made thereunder.

Application of other laws:

The provisions of this Act shall be in addition to and not in derogation of the provisions of any other law for the time being in force.

Power to Remove Difficulties:

If any difficulty arises in giving effect to the provisions of this Act, the State Government may, by order published in the Official Gazette, make such provisions, not inconsistent with the provisions of this Act, as may appear to be necessary for removing the difficulty:

Provided that no such order shall be made after the expiry of a period of two years from the commencement of this Act.

(2) Every order made under this section shall be laid, as soon as may be after it is made, before the State Legislature.

Observations and Personal viewpoints on the Fiscal Responsibility Act :

Observation:

The Gujarat government has been able to realise the targets it set out in the 2005 Fiscal Responsibility Act.

Viewpoint:

The Act is a necessary and essential measure for the State and National Governments to ensure that they are not pushed into fiscal deficit and are able to maintain revenue surplus which can then be utilized to provide goods and services for the public.

An important part of the Fiscal Responsibility Act is the escape clause which protects the government from criticism during adverse unforeseen circumstances.

Even though the act lays out the principles and directions for the government, the implementation is still not at the optimum level and certain changes in the Act will help to overcome the problems faced during implementation.

Amendments to the Act:

Most recently, in view of the Covid Pandemic and its adverse effect on the resources of the State Government, the Gujarat Fiscal Responsibility Act was amended in February, 2021 allowing the Gujarat State Government to raise additional resources by increasing the borrowing limit by 2% of the Gross State Domestic Product for the financial year 2020-2021.

Sources:

India Code:

https://www.indiacode.nic.in/handle/123456789/4367?view_type=search&sam_handle=123456789/2455

Gujarat Government Finance Department:

https://financedepartment.gujarat.gov.in/Documents/Act_10_2021-2-1_196.PDF

Indian Express:

https://indianexpress.com/article/india/gujarat-assembly-passes-3-bills-unanimously-7213176/

PRSIndia:

Live Mint:

Comments

Post a Comment